Meta Description: Master accounting for small businesses with this comprehensive guide. From basics and setup to expert tips and common pitfalls, empower your venture for financial success and growth.

Introduction

Running a small business is an exhilarating journey. It’s filled with creativity, innovation, and the thrill of building from the ground up. Still, amid the excitement, one critical aspect often gets overlooked: accounting. For solo entrepreneurs, freelancers, small retail owners, restaurant operators, and first-time founders, effective accounting is more than crunching numbers. It’s the backbone of sustainable growth. It helps track cash flow, comply with tax requirements, and support informed decision-making. These choices can mean the difference between thriving and merely surviving.

In this complete guide to accounting for small businesses, we’ll demystify the process and address common pain points. These include overwhelming tax calculations, reconciling bank statements, and generating profit-and-loss reports. Whether you’re a tech-savvy freelancer juggling invoices or a restaurant owner handling tips and payroll, understanding accounting helps you avoid penalties, maximize deductions, and clarify your business’s health. By the end, you’ll have the tools to handle your finances confidently or know when to seek professional help.

Accounting for small businesses doesn’t have to be intimidating. With the right approach, it can become a strategic advantage. Let’s move from the big picture to the basics.

Understanding the Basics

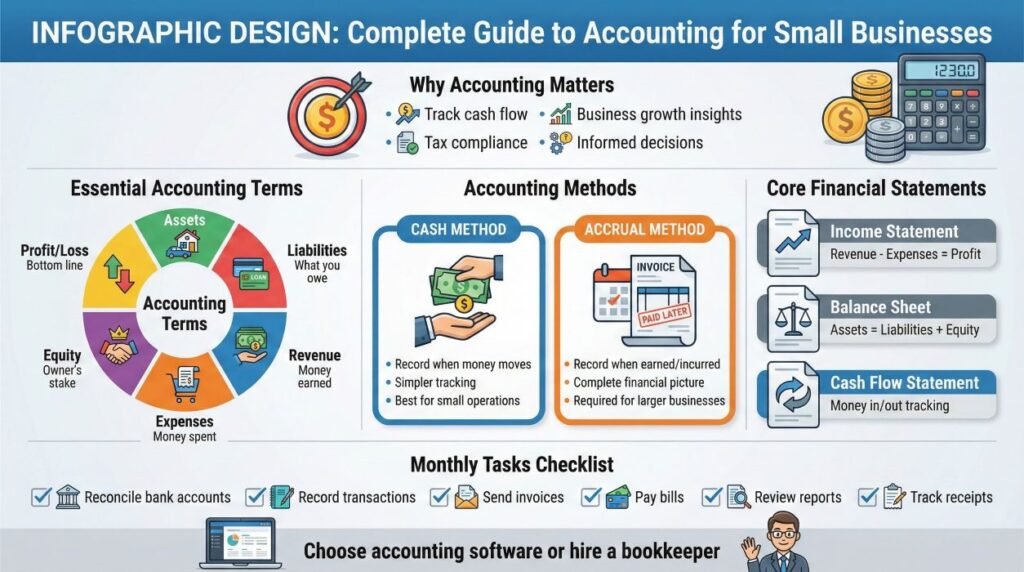

Before diving into complex strategies, it’s essential to grasp the fundamentals of accounting. At its core, accounting is the systematic process of recording, analyzing, and reporting financial transactions. For small businesses, this means keeping track of income, expenses, assets, liabilities, and equity to ensure everything adds up.

What is Accounting?

Accounting has two main methods: cash basis and accrual basis. Cash basis records transactions when money changes hands. This approach is simple for beginners but less accurate for long-term planning. Accrual basis records income and expenses when they’re earned or incurred. This gives a clearer picture of financial health. Most small businesses start with a cash basis. They often switch to accrual as they grow, especially if dealing with inventory or credit.

Key financial statements include:

- Balance Sheet: This is a summary of your business’s assets (what you own, like cash and equipment), liabilities (what you owe, such as loans and unpaid bills), and equity (the difference between assets and liabilities, representing ownership value). It helps assess whether your business can meet its financial obligations.

- Income Statement (Profit & Loss): Shows your business’s revenues (money earned), expenses (money spent), and net profit (what remains after expenses) over a specific period, revealing if you’re operating at a gain or loss.

- Cash Flow Statement: Tracks cash coming in (inflows) and going out (outflows), which is crucial for understanding how much readily available cash a business has (liquidity) and for ensuring the business does not run out of cash to pay its bills (cash shortages).

For target audiences like digital services freelancers, accounting basics mean categorizing gig payments and home-office deductions. Retail owners must handle sales tax and inventory costs, while restaurant operators deal with variable expenses such as food costs and tips.

Why Accounting Matters for Small Businesses

Poor accounting can lead to IRS audits, cash flow crises, or missed growth opportunities. According to the U.S. Small Business Administration, effective financial management helps track assets and liabilities, preventing surprises during tax season. With rising inflation and economic uncertainties, staying on top of finances is more vital than ever.

If you’re overwhelmed, consider user-friendly tools. For instance, QuickBooks offers intuitive features for beginners.

Key Considerations

When setting up accounting for small businesses, several factors come into play based on your industry and scale. These considerations ensure compliance, efficiency, and scalability.

Legal and Tax Requirements

Small businesses must comply with federal, state, and local taxes. Sole proprietors report on personal tax returns (Schedule C), while LLCs or corporations have separate filings. Key deadlines include quarterly estimated taxes (due on April 15, June 15, September 15, and January 15) and annual returns, due by April 15. Overlooking these can result in penalties up to 25% of unpaid taxes.

For e-commerce owners, sales tax nexus varies by state—track where you have economic presence. Restaurants face additional complexities with payroll taxes on tips, often requiring specialized software.

Choosing the Right Accounting System

Decide between manual spreadsheets, desktop software, or cloud-based platforms. Cloud options like Xero are ideal for tech-savvy users, as they offer real-time collaboration. Consider your needs: inventory tracking for retail, payroll integration for hospitality, or simple invoicing for freelancers.

Budget is key—free tools like Wave suit startups, but paid ones provide advanced features. Also, consider scalability: as your business grows, you’ll need systems that integrate with your CRM or e-commerce platform.

Hiring Help: DIY vs. Professional

Many first-time founders do their own accounting to save money. As complexity increases, it’s wise to outsource to a bookkeeper or CPA. Bookkeepers manage daily records. Accountants offer strategic advice. If overwhelmed by paperwork, professional help reduces errors.

A key consideration is data security—use encrypted tools to protect sensitive financial info.

Step-by-Step Guide

Here’s a practical, step-by-step approach to implementing accounting for your small business. Follow these to build a solid foundation.

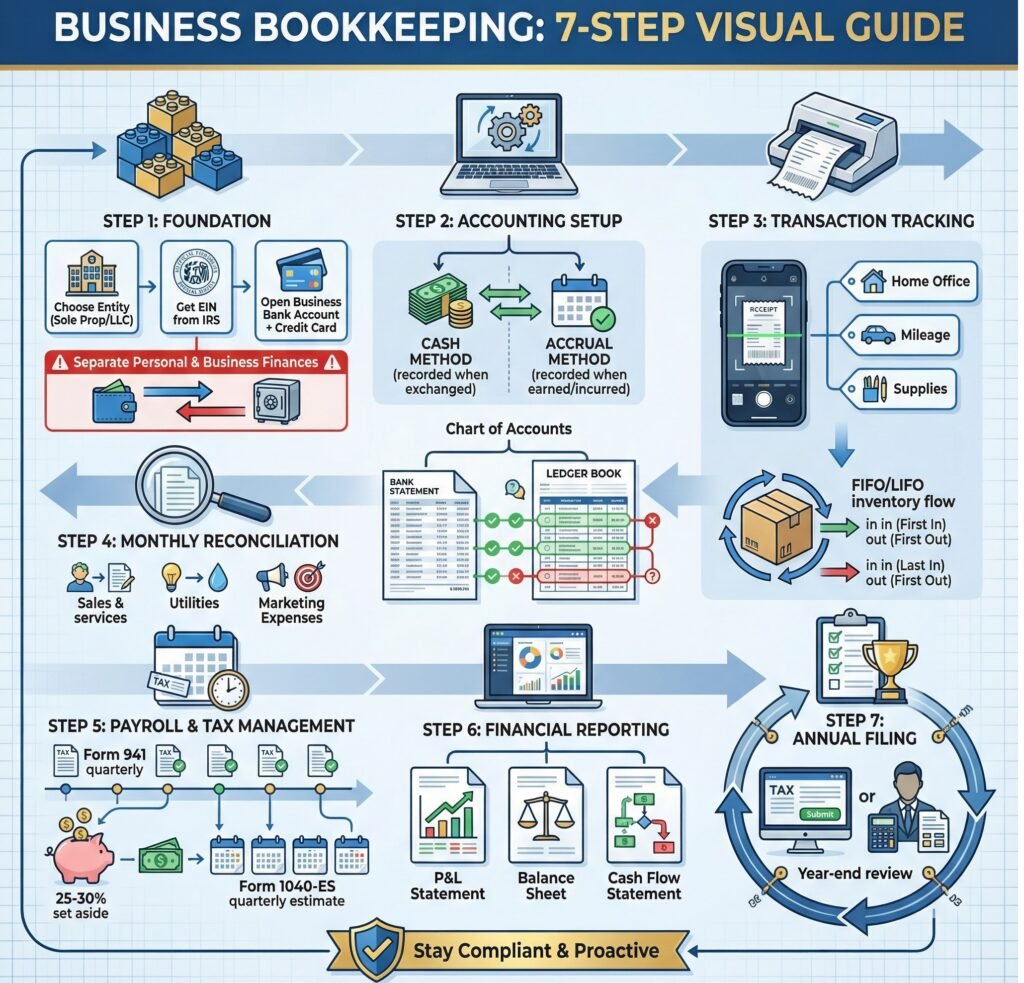

Step 1: Set Up Your Business Structure and Accounts

Choose your entity (sole proprietorship, LLC, etc.) and obtain an EIN from the IRS. Open a business bank account and credit card. Keep personal and business finances separate to avoid IRS red flags.

Step 2: Select Accounting Software and Method

Pick software based on your needs. For service-based businesses, FreshBooks excels in invoicing. Start your free FreshBooks trial now to streamline your billing.

Choose either the cash method, where income and expenses are recorded when money changes hands, or the accrual method, where income and expenses are recorded when they are earned or incurred, regardless of when money is exchanged. Set up a chart of accounts with categories such as revenue (money earned), utilities (payments for services like electricity and water), and marketing expenses (costs for promoting your business).

Step 3: Track Income and Expenses

Record every transaction promptly. Use apps to scan receipts. Categorize expenses for deductions, like home office for freelancers or mileage for deliveries.

For retail, implement inventory tracking using FIFO (First In, First Out) or LIFO (Last In, First Out).

Step 4: Reconcile Accounts Regularly

Each month, match your bank statements to your records. This helps catch discrepancies early and prevents fraud or errors.

Step 5: Manage Payroll and Taxes

If you have employees, withhold taxes and file Forms 941 quarterly. For hospitality tips, use software to allocate properly.

Estimate taxes quarterly using Form 1040-ES. Set aside 25-30% of your income for taxes.

Step 6: Generate Financial Reports

Produce monthly profit and loss statements, balance sheets, and cash flow statements. Analyze trends. If expenses rise, cut costs.

Step 7: File Taxes and Review Annually

Use tax preparation software or hire a pro. Review your year-end numbers for any needed adjustments.

Following these steps ensures you stay compliant and proactive.

Expert Tips

Drawing from industry experts, here are proven tips to elevate your accounting game.

Automate Where Possible

Start saving hours—try Xero for seamless automation today.

Perform Regular Checkups

Schedule weekly cash flow reviews and monthly deep dives into reports. This helps spot issues like slow-paying clients.

Budget Wisely

Create realistic budgets based on past data. Anticipate seasonal spikes, such as holiday surges for retail.

Maximize Deductions

Track mileage, home office use, and supplies. Use Section 179 for equipment write-offs.

Stay Educated

Follow SBA resources. Join communities such as Reddit’s r/Entrepreneur to stay updated on 2026 tax changes.

Backup Data

Cloud backups prevent loss from crashes.

These tips, from sources like QuickBooks and Forbes, can truly transform your finances.

Common Mistakes

Avoid these pitfalls that plague many small businesses.

Mixing Personal and Business Finances

This complicates taxes and audits. Always use separate accounts.

Poor Recordkeeping

Lost receipts mean missed deductions. Digitize everything.

Neglecting Reconciliation

Unreconciled accounts hide errors or theft.

Overlooking Cash Flow

Focusing solely on profits overlooks liquidity. Many businesses fail due to cash shortages.

DIY When Overwhelmed

Startups often skip pros, leading to costly mistakes.

Ignoring Tax Deadlines

Penalties add up quickly.

Inaccurate Categorization

Wrong expense labels reduce deductions.

By sidestepping these mistakes, as noted by Bench and Ramp, you’ll maintain accuracy.

To avoid errors, try Zoho Books. Start using Zoho Books to ensure integrated, error-free accounting.

Conclusion

Mastering accounting for small businesses is a game-changer, turning potential headaches into opportunities for growth. From understanding basics to implementing a step-by-step system, avoiding common mistakes, and applying expert tips, you’re now equipped to handle finances with confidence. Remember, it’s not about perfection but consistency and learning.

If you’re ready to automate, revisit our recommendations: QuickBooks for comprehensive features, FreshBooks for invoicing, Xero for collaboration, or Zoho Books for affordability.

Stay proactive, and watch your business flourish. For personalized advice, consult a professional. Here’s to your financial success!