Introduction

It’s midnight. Receipts are everywhere. A tax deadline looms. You started your business to chase your dream, not to become an amateur bookkeeper. If you’re a solopreneur, online store owner, or small business founder, you’re not alone—managing finances often stifles growth and steals joy.

You don’t have to do everything yourself or hire full-time staff. Outsourced accounting provides expert support at a fraction of the cost. But how do you pick the right partner among so many options? This guide helps you make your decision clear, confident, and focused on growth.

Now that you understand the benefits of outsourcing your accounting, let’s dive into the foundational concepts. Understanding what outsourced accounting truly means is key before you start evaluating your options.

Before diving into selection criteria, let’s clarify what modern outsourced accounting entails. It’s more than tax preparation or yearly bookkeeping. A full-service outsourced accounting firm acts as your dedicated, off-site finance department. They handle day-to-day transactions, produce financial statements, manage payroll, and ensure tax compliance. Often, they provide strategic advice to help you make data-driven decisions.

For a growing e-commerce store, this might mean integrating real-time sales data from Shopify, Amazon, and Etsy. For a local retailer, it could involve managing inventory, accounting, and sales tax across multiple jurisdictions. The core value is expertise, scalability, and insight—freeing you to focus on the work only you can do.

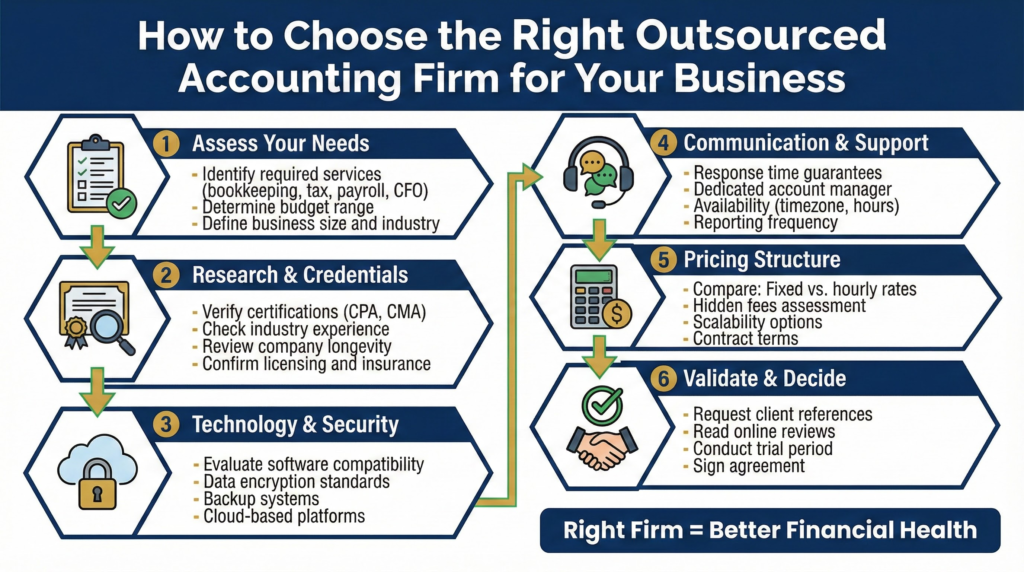

Key Considerations Before You Start Your Search

Not all accounting firms are created equal. Your ideal partner should align with your business’s needs, culture, and growth path. Here are the non-negotiable factors to weigh.

1. Industry-Specific Experience

An accountant familiar with your industry is worth their weight in gold. They’ll understand your key metrics, common deductions, and regulatory hurdles.

- For E-commerce/Dropshipping: Look for firms proficient in platform integrations (Shopify, WooCommerce), multi-channel sales tax (Nexus laws), and inventory costing methods.

- For Service-Based Solo Entrepreneurs: Seek expertise in project-based accounting, deductible home office expenses, and quarterly estimated taxes.

- For Startups: Find a firm fluent in burn rate calculations, cap table management, and R&D tax credits.

2. Range of Services Offered

Define what you need now and in the next 12-24 months. Core services typically include:

- Bookkeeping & Account Reconciliation

- Monthly/Quarterly Financial Reporting (P&L, Balance Sheet, Cash Flow)

- Tax Preparation & Planning (Income, Sales, Payroll Taxes)

- Payroll Processing

- Advisory Services (Budgeting, Forecasting, Financial Analysis)

Choose a firm that can grow with your business. Start small if needed, but make sure they offer deeper advisory services for when your needs evolve.

3. Technology Stack & Integration

Your firm should be tech-forward. They should use a secure, cloud-based accounting platform, such as QuickBooks Online or Xero. This gives you real-time access to your financial dashboard. Their systems must also integrate seamlessly with your existing tools: your point-of-sale system, payment processors, and banking apps. Ask about their data security protocols.

Want to see what best-in-class cloud accounting looks like? Check out our detailed review and exclusive partner discount for QuickBooks Online, the platform trusted by most top accounting firms.

4. Pricing Structure & Transparency

Understanding how you’ll be billed prevents nasty surprises. Common models include:

- Fixed Monthly Fee: Best for predictable workloads and budgeting.

- Hourly Rate: May be suitable for very limited, irregular needs.

- Tiered Packages: Bundle services at different price points.

Insist on clear contracts that outline exactly what’s included, response times, and costs for ad-hoc requests.

5. Communication & Company Culture

This is a partnership. You need a firm that communicates in plain English, not only accounting jargon. Do they offer regular check-in calls? Will you have a dedicated account manager? Do their values and responsiveness match your expectations? A firm that feels like an extension of your team is the ultimate goal.

Your Step-by-Step Guide to Selecting a Firm

Follow this actionable process to narrow your options and make a confident choice.

Step 1: Conduct an Internal Assessment

Identify your major pain points and what you want improved. Know your budget and technology stack, so you can approach firms confidently and compare solutions.

Step 2: Research & Create a Shortlist

Seek recommendations from your business network. Browse reputable online directories and read verified reviews. Look for firms that explicitly mention your industry or business size. Create a shortlist of 3-5 potential firms.

Step 3: Vet Their Expertise & Compatibility

Visit their websites. Review client testimonials and examine their service pages. Do they publish content relevant to your challenges? This demonstrates thought leadership. Check for relevant credentials, such as CPA or CA.

Step 4: Schedule Initial Consultations

This is the most critical step. Prepare a list of questions for your discovery calls:

- “Can you walk me through your typical client onboarding process?”

- “How do you handle communication and reporting?”

- “Can you provide a case study or example of how you’ve helped a business like mine?”

- “What is your pricing structure for a business with my transaction volume and needs?”

- “What’s your process at tax time?”

Gauge their curiosity about your business. A good firm will ask as many questions as they answer.

Step 5: Check References & Make a Decision

Request 1-2 references from similar-industry clients. Ask about reliability, problem-solving, and achieved value. When comparing proposals, weigh total value—expertise, technology, service fit—and trust your instincts on a partnership.

Expert Tips for a Successful Partnership

- Start before you’re under pressure. Onboarding is faster and less stressful when you’re not facing deadlines or emergencies.

- Grant Proper Access: Ensure your new firm has “view-only” or appropriate access to your bank accounts, merchant processors, and sales platforms. Transparency is key to accurate books.

- Establish Clear KPIs: Beyond clean books, define what success looks like. Is it better for cash flow forecasting? Higher tax savings? Monthly profit & loss reviews? Align on goals upfront.

Common Mistakes to Avoid

- Choosing on Price Alone: The cheapest option can be the most expensive. They may make errors or offer no strategic insight.

- Ignoring the Tech Fit: If they use outdated, desktop-only software, you’ll lose the real-time visibility you need.

- Not Defining Scope: Vague agreements lead to scope creep and unexpected bills. Get everything in writing.

- Stay involved even after outsourcing. Review reports, ask questions, and participate in planning to keep full control over your financial direction.

Avoid the #1 mistake—poor record-keeping. Streamline your financial data with this guide to the best business expense tracking tools, recommended by financial professionals.

Conclusion

Choosing the right outsourced accounting firm shapes your business future. Look for a partner who protects compliance, optimizes tax, and enables growth. Use this guide’s steps: check industry expertise, tech capability, and communication. A structured process overcomes errors and DIY headaches.

Reclaiming your time and gaining strategic insight will yield greater returns than your initial investment. To begin: clarify your needs, research your options, and initiate conversations. This sets you up for a future where you are relaxed, informed, and focused on growth.

Ready to take the next step, but want to get your own financial snapshot first? Sign up for a free trial of leading accounting software and generate a professional profit & loss statement to bring to your first accountant consultation.

Meta Description: Struggling with books & taxes? Learn how to choose an outsourced accounting firm. Get expert tips for solopreneurs, e-commerce & small biz owners.