Meta Description: Discover essential tips for outsourcing small biz accounting. Learn how to select the best firm to save time, reduce costs, and avoid tax errors for your growing business.

Introduction

Running a small business is exhilarating, but financial management is often overwhelming. Whether you’re a solo entrepreneur, an e-commerce store owner, a brick-and-mortar retailer, or a startup founder, accounting tasks add up fast. Hiring a full-time accountant is costly and time-consuming, making outsourcing small-business accounting a decisive, cost-effective solution.

By outsourcing your accounting to specialized professionals, you can dedicate more energy to business growth while experts handle your finances. But with numerous firms to choose from, selecting the right partner is critical for success. This guide shows you how to confidently choose a firm that matches your goals and budget.

This article addresses common pain points: in-house costs and complexity, concerns about tax errors, and limited time. Whether you are a freelancer, service provider, or small business owner facing growing bookkeeping burdens, smart outsourcing offers a scalable, cost-effective path forward.

Understanding the Basics

Before you choose a provider, understand what outsourced accounting is and why it’s common among small businesses.

What Is Outsourced Accounting?

Outsourced accounting involves delegating your financial tasks to an external firm or service provider. This can include bookkeeping, payroll processing, tax preparation, financial reporting, and even strategic advice, such as cash flow forecasting. Unlike traditional in-house accounting, outsourcing leverages a team of professionals who use cloud-based tools to manage your books remotely.

For instance, if you’re a dropshipping store owner managing sales on Shopify, Amazon, and Etsy, an outsourced firm can integrate these platforms to provide real-time financial insights. This eliminates the need for you to manually reconcile transactions, saving hours each week.

Benefits of Outsourcing for Small Businesses

The advantages are numerous, particularly for the target audiences mentioned. Solo entrepreneurs and freelancers often operate on tight margins, making the affordability of outsourcing appealing—firms charge based on usage, often starting at $200-$500 per month, far less than a full-time salary of $50k+ annually.

E-commerce owners benefit from specialized expertise in handling multi-channel sales tax compliance, which can be a nightmare if done DIY. Brick-and-mortar businesses, such as local retail shops, appreciate the reduction in paperwork, allowing owners to focus on customer service. Startups in growth phases find outsourcing scalable; as your revenue climbs from $50k to $250k, the service can expand without hiring disruptions.

Moreover, outsourcing mitigates risks like tax filing errors. According to a study by the IRS, small businesses underreport income or overclaim deductions in about 20% of cases, leading to penalties. Professional firms stay up to date on tax laws, ensuring compliance and maximizing deductions.

When Should You Consider Outsourcing?

If you spend over 10 hours a month on accounting, face cash flow surprises, or dread tax season, outsourcing is worth considering. Early signs include messy receipts, late invoices, or the use of error-prone spreadsheets. Startups prevent blind spots by outsourcing early.

Key Considerations

Choosing an outsourced accounting firm depends on your business’s unique needs.

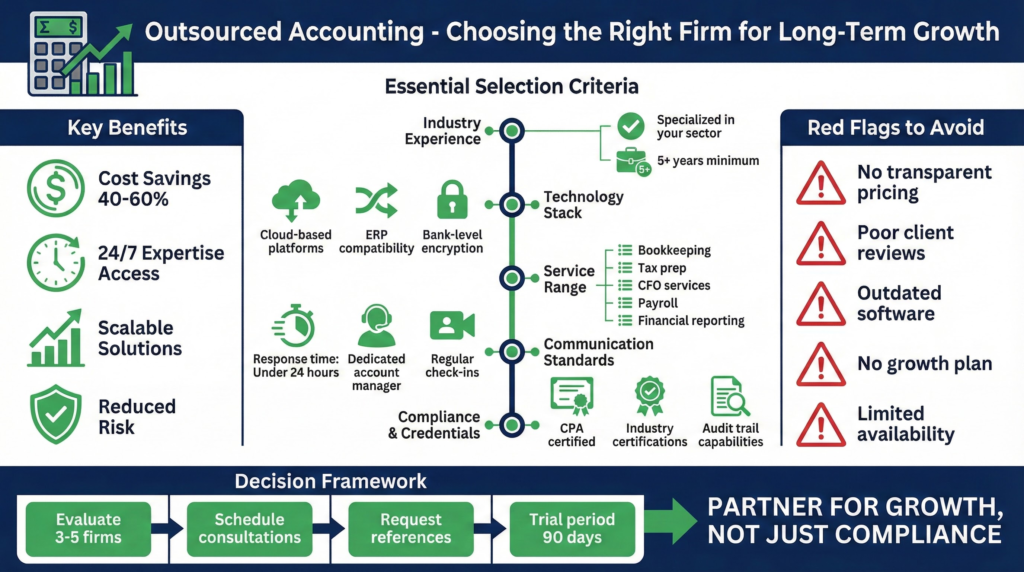

Industry Expertise and Specialization

Not all firms are created equal. Look for those with experience in your sector. For e-commerce owners, a firm familiar with platforms like Shopify or WooCommerce is ideal. Freelancers might need expertise in 1099 forms and self-employment taxes, while brick-and-mortar stores require knowledge of local sales tax variations.

Ask if firms have clients like you. A startup-specialized firm will understand venture funding and equity needs.

Technology and Tools

In today’s digital age, the right tech stack is non-negotiable. The firm should use cloud-based software such as QuickBooks Online, Xero, or FreshBooks to enable seamless collaboration. This allows real-time access to your financial data via mobile apps, perfect for tech-savvy entrepreneurs on the go.

Ensure they prioritize data security through encryption and compliance with standards such as SOC 2. For multi-channel e-commerce, integration with tools like Stripe or PayPal is essential to automate transaction tracking.

Pricing Models and Transparency

Firms may offer flat rates ($300-$1,000/month), hourly rates ($50-$150/hour), or charge by transaction. Watch for hidden fees on add-ons like tax filing.

Transparency is key—request a detailed quote upfront. For small businesses with revenues under $250k, aim for services that scale with growth to avoid overpaying in the early stages.

Communication and Support

How responsive is the firm? As a busy owner, you need timely answers. Look for dedicated account managers, regular check-ins (weekly or monthly), and 24/7 portals for queries.

Cultural fit matters too. If you’re a 30-something freelancer, a firm with a modern, approachable vibe might suit you better than a corporate giant.

Certifications and Reputation

Verify credentials, such as CPA (Certified Public Accountant) status, for tax expertise. Check reviews on platforms like Trustpilot or Clutch. A firm with a 4.5+ rating and testimonials from similar businesses is a good sign.

Step-by-Step Guide

Now that you understand the basics and key factors, here’s a practical, step-by-step process for selecting and onboarding the right firm.

Step 1: Assess Your Needs

First, evaluate your existing accounting setup. List specific tasks like bookkeeping, payroll, or taxes that take up the most time or cause the most frustration. Note exactly how many hours you spend monthly and the types of errors that have occurred recently.

For example, if cash flow blindness is an issue, prioritize firms offering forecasting services. E-commerce owners should list integrations needed.

Step 2: Research Potential Firms

Next, use online directories such as Upwork, Clutch, or Google to search for ‘outsourced accounting for small businesses.’ Create a shortlist of 5-10 firms based on relevant reviews and demonstrated experience in your industry.

Consider affiliate-recommended services for reliability. For instance, Bench.co offers tailored bookkeeping for small businesses—sign up here for a free trial and get your first month free.

Step 3: Request Proposals and Quotes

Contact each firm on your shortlist and send a detailed Request for Proposal (RFP) outlining your business type, annual revenue, current accounting tools, and pain points. Carefully compare the quotes you receive to ensure fair comparison.

Ask about turnaround times—e.g., monthly reports within 5 business days.

Step 4: Conduct Interviews and Demos

Schedule calls or product demos with your top candidates. Ask questions based on scenarios similar to your business, such as quarterly taxes for freelancers or multi-state sales tax for e-commerce. Observe how each firm handles your questions and their approach to real cases.

Test their tech: Request a demo of their dashboard.

Step 5: Check References and Contracts

Request references from 2-3 current clients of each shortlisted firm. Ask those clients about the firm’s reliability, attention to detail, and quality of customer support. Use their feedback to make your final comparison.

Review contracts carefully: note all terms, cancellation (at least 30 days), and confirm your data ownership.

Step 6: Onboard and Monitor

When you select a firm, provide necessary access to your financial accounts and set specific, measurable goals, such as zero errors in monthly reports or improved cash flow tracking.

Check monthly for issues and address them without delay.

Expert Tips

To maximize the value of outsourcing small biz accounting, heed these insights from industry pros.

Tip 1: Start Small

Start with bookkeeping, then add more services as trust grows—this reduces risk.

Tip 2: Leverage Automation

Choose firms that use AI-driven tools for efficiency. For example, Pilot.com integrates automation to speed up reconciliations—explore their plans and save 20% on your first year via this affiliate link.

Tip 3: Focus on Scalability

Ensure your firm can manage growing complexity, like international e-commerce.

Tip 4: Integrate with Your Workflow

Connect with your current tools. If you use Trello, choose a firm that sends reports there.

Tip 5: Stay Involved

Stay involved—review reports monthly to stay informed about your business.

For comprehensive software integration, consider QuickBooks Online partnered with outsourced services.

Common Mistakes

Avoid these pitfalls to ensure a smooth outsourcing experience.

Mistake 1: Choosing Based Solely on Price

Cheapest firms may lack expertise, leading to costly mistakes. Balance cost and value; a somewhat pricier firm can save thousands in taxes.

Mistake 2: Ignoring Data Security

Today’s cyber threats demand strong security. Always verify HIPAA or GDPR compliance if needed.

Mistake 3: Poor Communication Expectations

Don’t expect 24/7 support without confirmation. Set clear SLAs (Service Level Agreements) early.

Mistake 4: Not Reviewing Contracts Thoroughly

Hidden clauses, like auto-renewals, can trap you. Have a lawyer skim if needed.

Mistake 5: Delaying the Switch

Procrastinating due to fear of change exacerbates disorganization. Start early for tax season prep.

To sidestep these, try Bookkeeper360, which offers customizable plans—claim your free consultation and 10% off initial setup.

Conclusion

Choosing the right outsourced accounting firm can transform your business operations, freeing you from financial drudgery so you can pursue growth. By understanding the basics, weighing key considerations, following a structured guide, applying expert tips, and steering clear of common mistakes, you’ll find a partner that alleviates your pain points—high in-house costs, tax fears, and time shortages.

Remember, outsourcing isn’t just about delegation; it’s about gaining strategic insights for better decisions. Whether you’re a freelancer streamlining deductions or a startup scaling efficiently, the right firm is out there.